AFL Position Is Inconsistent with the Government of Canada

Despite the fact that the Charity does not engage in foreign activities, the AFL makes an effort to connect the Charity with international organisations or events.

In referring to global events, international organizations, and certain countries, the AFL makes allegations that are inconsistent with Government of Canada and are influenced by political viewpoints, particularly some that are rooted in anti-Muslim sentiments.

Taking the Syrian revolution as an example, the AFL is concerned about unsolicited emails that express support and solidarity with the Syrian people in the struggle to oppose the aggression of the Syrian Regime and Bashar Al Assad.

The Free Syrian Army (FSA) was founded by Syrian military defectors who refused to attack peaceful protestors on the orders of Bashar Al Assad. Canada has given $5.3-million to the Syrian opposition to support the rebels in anti-government propaganda since April 2012, according to the Department of Foreign Affairs (DFAIT).114 In May 2013, the European Union lifted a 2011 arms embargo on Syria. Several EU members wanted to be able to send weapons to rebel groups in order to speed up regime change and oust Bashar al-Assad. Since then, France, the United States, Qatar, Saudi Arabia, Turkey and others, have provided arms to the FSA. The Syrian National Council (SNC) was recognised or supported in some capacity by 17 UN member states, with three of those being permanent members of the Security Council as the legitimate representative of the Syrian people in the midst of the Syrian Civil War. It was also recognised by the European Union, the International Union for Muslim Scholars, and the Arab League.115 Foreign Minister John Baird, in a December 16 2011 speech in the House of Commons stated, “Assad will fall. The government will fall. It’s only a matter of time”. Later that day, Baird met with a Syrian National Council delegation led by Council President Burhan Ghalioun. The council expressed its gratitude for Canada’s assistance to the SNC, including international lobbying for new UN Security Council resolutions and its rejection of the Assad government. Discussions were held on Canada’s participation in humanitarian assistance during a transitional period and in the rebuilding of a post-Assad Syria.116 Foreign Affairs Minister John Baird expanded sanctions to include 22 more individuals associated with the Assad regime and seven companies.117 The AFL raises concern why the Organization would receive unsolicited emails that discuss the apparent involvement of the Syrian Muslim Brotherhood and the FSA in the violence occurring in Syria. The CRA’s partisan view of these groups is inconsistent with the diplomatic role of the Canadian government.

When it comes to Palestine, the AFL expresses concern regarding remarks made by individuals, rather than the Charity, in opposition to the occupation of Palestine and human rights violations committed by the State of Israel. Global Affairs Canada has always maintained a consistent foreign policy towards Palestine and Israel. The Ministry states “Canadian foreign policy objectives in the Middle East are the foundation for international assistance programming in the West Bank and Gaza.

Canada is committed to the goal of a comprehensive, just and lasting peace in the Middle East. This goal supports the creation of a viable, independent and democratic Palestinian state living side by side in peace and security with Israel. Canada believes that peace can only be achieved through a two-state solution negotiated directly between the parties.”118 The Government of Canada at the United Nations has voted in favor of the right of the Palestinian people to self- determination.119

Furthermore, the AFL relies upon comments made by the Egyptian Embassy in Canada to support its conclusions, particularly on sections related to the Egyptian revolution and Egyptian pro-democracy groups. The Egyptian Embassy is an extension of the Egyptian regime, which is responsible for overthrowing a democratically elected president and the massacre and torture of civilians. Two large sit-ins in Cairo and smaller protests across Egypt took place to denounce the military takeover and demand the reinstatement of President Morsi. In response, it is this same Egyptian government that ordered forces to repeatedly open fire on demonstrators, killing over 1,150. It is the worst massacre in Egyptian history.120

Furthermore, the Egyptian Embassy in Ottawa is also responsible for bringing and hosting Egyptian Minister Nabila Makram in Canada, who told an audience in Mississauga, Ontario, that anyone speaking “against Egypt abroad” will be “punished.” A video of Makram’s comments shows her making a slicing motion across her neck while making the remark.121 This comes after Egypt’s well documented record of arbitrary detentions, violence against political opponents and other human-rights abuses since General Abdel Fattah al-Sisi (who was famously referred to by President Trump as “my favorite dictator”122) seized power via a military coup.

In response to this incident Canada’s then former Foreign Affairs Minister Chrystia Freeland stated “Canada continues to support the desire of the Egyptian people for democracy, human rights, the rule of law and greater economic opportunity. The rights to free speech and expression are fundamental to democracy and our government will always defend Canadians – and people around the world – in their ability to exercise these rights.”123

The CRA should have exercised greater caution rather than relying on reports from a foreign government with such an atrocious record of brutality against its own citizens and whose state-controlled media outlets routinely portray Muslim community groups in the West as a threat.

2015 Board Retreat

The AFL relies extensively on the minutes of a September 2015 “Board Retreat,” yet it misrepresents both the context, the discussion and outcomes of this meeting.

First of all, this was not a Board Retreat. It was a meeting called by the Board of Directors and a cross section of members based on background, gender, age, etc. were selected to participate. The meeting invitation states

The Board of Directors has invited you to participate in a retreat to engage in both a broad and an in-depth discussion regarding our Islamic presence in the current environment. The need for such a discussion is precipitated by ongoing public relations issues facing the organization. We have ongoing issues with negative media reports and a changing political environment. We are being defined by others rather than by ourselves.” (Sent by the chair of the Board to the attendees.)

The minutes reflect a Strengths, Weaknesses, Opportunities, and Threats (SWOT) brainstorming exercise of challenges and threats. Considering the domestic and foreign anti-Muslim campaigns that the Charity was experiencing at the time, and the actions taken by the UAE to list Muslim civil society organizations in the West as terrorist groups, it would have been either extremely naive or unconscionably irresponsible of the leadership of the Charity to not address the reputational risk to the organization. To be very clear, attendees of the retreat were not worried about the Charity being listed as a terrorist organization in Canada, rather the impact of Islamophobia on the organization.

Organizing a retreat to examine the Charity’s internal and external communications around the relationship with the Muslim Brotherhood and the nuances of referring to the organization versus referring to the movement versus referring to the thought and ideas, was and is the minimum appropriate action to be taken in this regard.

The retreat was informed by both legal and public relations advice. Both advised the Charity that the international characterization of the Muslim Brotherhood organization, even with no links to MAC, would have ramifications due to shared ideology. It is ironic that CRA raises concern about this retreat and its scope in the context of “failure to conduct due diligence” because the primary objective of the retreat was to ensure due diligence.

The Charity has never been concerned about its activities with regard to the criteria for being listed as a terrorist organization. The Charity has always been concerned about the domestic and foreign Islamophobia campaigns that could impact it in Canada or abroad. The Charity was in fact transparent with CRA and communicated several times, as explained earlier and confirmed through ATIPs, that the Charity was available to discuss with the CRA the false media stories and the Islamophobic reports that were being published.

The AFL also states at page 18 that, “The decision to focus on the core ideas of Imam Al-Banna as opposed to the Muslim Brotherhood philosophy appears to be a decision made at the September 12-13, 2015 Board of Directors retreat.” This was never a decision at the retreat. The meeting did not have the authority to make any such decision. Also, the scope of discussion was around articulation and not changing the Charity’s roots and identity. The minutes of the retreat were not formal and not approved by the Board. Many of the noted comments in the minutes were simply the opinion of attendees in the context of a discussion and were not necessarily points of consensus. There were many other points of view, and this was only one attendee’s point of view. However, the conclusions were taken back to the Board for consideration.

Having said that, the CRA had the agenda of the meeting which clearly stated the subject for discussion in the 2nd agenda item which stated, “Given the current national and international environments, do you see our definition of “who are we” causing serious internal or external challenges in terms of misunderstanding, wrong interpretations, political or public media pressures.” The AFL extracted the above text from the minutes and removed it from its original context. The minutes state “There was some apprehension about us not continuing to include HB and/or MB in our identity definition as, the argument goes, it would eventually lead to the eventual diminishment of our core values and principles.” The discussion was never about concern about activities that are problematic, or removing connections to external organizations, but about how to effectively describe the Charity with respect to the Muslim Brotherhood in its website, bylaws, and other publications.

The opinion developed by the CRA in the AFL concerning the retreat demonstrates a misconstrued and manifestly unfair approach to the audit. The retreat was called in fact to ensure due diligence and provide clarity to internal and external stakeholders. Recommendations were acted upon by the Board with transparent changes to the bylaws, the website and other materials. This process should have provided CRA with confidence that the Charity was taking necessary steps to ensure that the organization and how it articulates itself is in accordance with public policy.

Anti-Terrorism Policy (ATP)

In the summary found at page 58 the AFL states

“After a review of the Organization’s records and representations, the CRA found that despite having created an Anti-Terrorism Policy (ATP) in 2011, it appears as though the Organization never implemented the document in a truly meaningful manner and has failed to demonstrate that it conducts meaningful due diligence. The failure to conduct due diligence, whether purposeful or negligent, has resulted in several of the Organization’s activities being considered by the CRA to be activities contrary to public policy.”

The Charity developed its first Anti-Terrorism Policy and further developed an Adherence and Due Diligence Package which is current as of December of 2015.

This package outlines the Charity’s policies and position on various issues, including Anti- Money Laundering and Terrorist Financing. Relevant sections of this Package are as follows:

Extremist ideologies are inconsistent with our values as Canadian Muslims. Through our efforts to promote civic awareness and duty we try to educate and train our youth to bring positive change, thwarting the efforts of radicalization across the country.

The Charity operates a number of full-time schools across the country, preaching moderation and the contemporary practise of Islam. These schools have a strong curriculum approved by Governments across Canada.

The Charity is committed to the safety of its premises, students, staff, members and visitors and above all compliance with all relevant laws.

The Charity has developed policies, practises and procedures related to Anti-Terrorism, to ensure that the above commitment is being met.

The Charity is also committed to working with stakeholders in Government law enforcement and other faith groups to improve on these procedures. The Charity will continue to update these policies and procedures to ensure they remain current, effective and aligned with any new laws.

The MAC Anti-Terrorism Policy includes the following:

General Policy Guidelines and Principles

Risk Management

Governance Accountability and Transparency

Reporting

Program Review

Donor Review

Financial Transparency

Review of Participants

Review of Associates

Proceeds of Crime (Money Laundering) and Terrorist Financing Act

An Anti-Terrorism checklist was also developed to ensure that programs undertaken by MAC do not compromise its charitable status by contravening Anti- Terrorism Legislation. In this respect, a program under review should not involve or appear to involve the association with terrorist activities, terrorist groups or in facilitating terrorist activities or terrorist groups. MAC has provided a copy of an Anti-Terrorism Due Diligence Program Review conducted in the audit period attached again at Schedule “23”.

The Charity has in fact applied its anti-terrorism policy using an objective approach in judging a group’s risk based on legitimate reliable sources, specifically the Canadian, US, EU, and UN terrorist lists, rather than online hearsay, third party sources, and misinformation. This is important to ensure that the Charity does not prejudice an organization doing important work. It is unreasonable for CRA to expect a charity to investigate “perceived links”, as the Charity can only rely on accessible government resources and reliable third-party providers to determine legitimate links to terrorist activities.

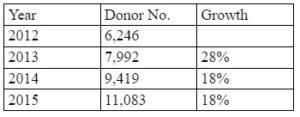

It’s important to note that the Charity’s donor community grew by 28% in 2013, 18% in 2014, and 18% in 2015 as shown below. These accounted for thousands of donation transactions. The AFL has not pointed out a single transaction or donor that it is concerned about for risk or identified “perceived links” despite the large number of donors and transactions.

At page 40, the AFL notes, “In order to prevent the charity’s resources from being used in a manner that would contravene Canadian law and the charity’s requirements for ongoing registration, a registered charity should conduct meaningful due diligence on all aspects of its operations. This would include ensuring that a charity does not operate in association with individuals or groups that are engaged in terrorist activities or that support terrorist activities. Links, alleged or even perceived links between a charity and terrorism are corrosive to public confidence in the integrity of charity. A significant aspect of a trustee’s legal duties to protect charitable assets means carrying out proper due diligence to give reasonable assurance about those individuals and organizations that give money to, or receive money from, or work closely with, the charity.”

First of all, it is unclear to the Charity why the CRA would reference the UK Charities Commission Guidance “OG 410 Charities and Terrorism” in explaining the Charity’s responsibility to ensure it does not contravene Canadian law and the charity’s requirements for ongoing registration. As a strictly domestic Canadian registered charity, the organization is not responsible to seek guidance or compliance with Charity regulators of foreign countries.

Nevertheless, in 2011 the Charity’s Board of Directors approved the Charity’s Anti-Terrorism policy to protect the Charity’s assets from abuse. The policy accounts for those individuals and organizations that give money to, or receive money from, or work closely with, the charity.

As it relates to donors the Charity’s policy requires that “A reasonable sampling of all new or proposed donors or donations less than $10,000.00 shall be subject to an initial review. All new or proposed donors or donations greater than $10,000.00 shall be subject to an initial review, and all existing Donor-lists shall be subject to review as required.” This policy has been implemented by MAC and demonstrated to the CRA.

In our letter of December 21, 2018 attached as Schedule “11”, the following clarification was provided:

“During the course of the head office visit between February 29, 2016 and March 1, 2016, questions were raised concerning the application of MAC’s anti-terrorism policy. At that time, the audit interview notes reflect that the executive director appeared to indicate that anti-terrorism policy is not consistently applied. For certainty, MAC is consistent in the application of the anti-terrorism policy in the course of its activities. This is applied across the entire organization, and is monitored and managed by the head office…

In relation to the fundraising activities of MAC discussed above, all donors and donations are subject to review by the anti-terrorism committee (currently made of the Director of the Fundraising, the Controller, and the Executive Director) to determine, to the extent possible, whether they are compromised by any connection or appearance of connection with Terrorist Activity, Terrorist Groups, or Facilitating Terrorist Activity or Groups or whether they may be otherwise in violation of the Anti-Terrorism Legislation, including the Proceeds of Crime (Money Laundering) and Terrorist Financing Act.

All donor reviews, whether of new or existing donors, are conducted in accordance with the Donor Review Check-List attached to MAC anti-terrorism policy as per Schedule C. Therefore, all donors making donations of $10,000 or more are screened against a variety of international and country-sponsored Watch lists, while donations of less than $10,000 are sample-screened through a randomized sampling.

A reasonable randomized sampling (about 1 % of transactions) of all donors or donations less than $10,000.00 are subject to similar checks and reviews.

No positive identification has occurred to date. However, in the event that a donor or donation is compromised by real or possible links to Terrorist Activities or Terrorist Groups, MAC shall not accept the donation, or any further donations as the case may be, from the donor. The donation shall be returned to the donor along with a brief explanation that MAC is unable to accept the gift where possible at law after consultation with legal counsel. MAC shall keep a copy of the documentation, concerning the donation, on file.

Further, our client has provided the Canada Revenue Agency Auditors a list of checks that the organization performs based on the individual’s role in the organization.”

This clarification has effectively been ignored by the CRA.

Povrel Jerusalem Fund for Human Services (JFHS) and The Canadian Middle East Information Centre (CMIC)

The Charity is concerned about the CRA including allegations against The Canadian Middle East Information Centre (CMIC) of spreading propaganda that have never been proven. The CRA bases its allegation on the fact that in an Immigration Refugee Board (IRB) process the “CMIC acknowledged that it distributes two Islamic newspapers.” (Appendix F) This is in fact not true.

Referring to the original text of the IRB testimony, the allegations presented before the IRB are by an unknown source and not by CMIC.124 There is nothing provided to support the allegations made by the CRA.

As it relates to the Povrel Jerusalem Fund for Human Services (JFHS), CRA’s accusations concerning the relationship between JFHS and IRFAN-Canada is simply an attempt to draw some degree of influence on the Charity between it and IRFAN-Canada.

The AFL alleges at page 45 that

“As detailed in Appendix F, some of the Organization’s most prominent members, directors, and officials were either involved in IRFAN-Canada, or a network of charities that appear to have been used to propagate and fundraise for Hamas in Canada. The involvement of the directors/employees in an apparent Hamas support network is troubling and may indicate why certain activities, such as the continued support for IRFAN-Canada, were undertaken by the Organization.”

The CRA in this appendix attempts to demonstrate that since some individuals associated with the Charity served as board members with JFHS or CMIC prior to 1999 and before MAC was ever registered, it is evidence that there existed influence on the Charity to provide support/resources to IRFAN-Canada a decade later. The members of the Charity have always been active members in their community. It should be no surprise that they are active in other organizations within the community before and after the Charity was founded. The linking of individuals or directors who served or serve on other organizations to allegations of influence on the decisions, policies, and activities of the Charity is completely speculative.

The Charity has never interacted with JFHS or CMIC. It interacted strictly with IRFAN-Canada, which was not listed by Canada, the US, the EU or the United Nations as an organization of concern until 2014.

Support for International Relief Fund for the Afflicted and Needy (IRFAN- Canada)

At page 45 of the AFL, the CRA alleges that, “An analysis of audit documentation and publicly available sources suggests that the relationship between the Organization and IRFAN-Canada not only continued after the suspension of IRFAN-Canada’s registered status but well after its revocation for, in part, supporting the listed terrorist entity Hamas.” As well, on pages 45 and 46 CRA states that, “In addition to permitting IRFAN-Canada to use the Organization’s events and resources to collect funds, the Organization’s electronic resources appear to have been used to further IRFAN-Canada’s interests and agenda.” and “The Organization appears to have held several events where IRFAN-Canada was given an opportunity to promote itself and raise funds for its various programs.”

As explained, MAC’s institutions are used by the community and open to the community for external activities, for example community iftars, Eid gatherings, baby shower sermons, and other gatherings. This is similar to other faith groups.

Between 2011 and 2014 IRFAN-Canada remained a non-qualified donee as a non- profit organization. As a non-qualified donee, IRFAN-Canada rented MAC’s Olive Grove School and was allowed to hold an event by paying fees. Olive Grove School did not routinely rent out its building at the time, and as a result, its rental practice required community groups using the facility to cover the costs connected with the facility’s upkeep and cleaning directly with the cleaning company. To be clear, this permission was withdrawn as soon as IRFAN-Canada was included on the government of Canada’s list of terrorist organizations in April, 2014.

In other instances, IRFAN-Canada paid sponsorship fees to support the Charity’s events and in return received acknowledgement for its sponsorship. The ITA does not restrict a non-qualified donee from using the resources of a registered charity for fair market value. During this period in which it was a non-qualified donee, IRFAN-Canada has never raised funds in the Charity’s facilities or events. As noted above, the AFL references a YouTube video but the link provided is incorrect and cannot be verified. Also, the event links provided by the CRA in footnotes 222 and 223 are broken. While the Charity cannot verify the event description provided by the CRA, the Charity can confirm that the IRFAN-Canada was never allowed to, nor did it, fundraise in its Annual Grand Souk of Jerusalem event.

After December 2010 when the CRA revoked IRFAN-Canada’s charitable status many major Canadian organizations continued to affiliate with the organization. In 2011 and 2012 IRFAN-Canada remained a major sponsor of the Reviving Islamic Spirit Conference as well as one of the largest Muslim festivals, MuslimFest. Other Canadian mosques, of which some are registered charities, were renting their facilities to IRFAN-Canada for events. The City of Mississauga continued to rent its facilities to IRFAN-Canada for community picnics and events. In 2013 IRFAN- Canada in cooperation with The International Islamic Youth League, the United Nation High Commissioner for Refugees, the Zakat Foundation of America, the United Arab Emirates Red Crescent Society, and the Islamic Foundation of Ireland partnered to distribute humanitarian relief support to the refugees in Mali to support internally displaced persons.

The Charity rejects the conclusion that it allowed IRFAN-Canada to raise funds at real property owned by the Charity. IRFAN-Canada has never been allowed to fundraise in MAC premises. On page 46 of the AFL, the CRA raises 4 alleged incidents where this may have been the case. As a grassroots organization with access to the community, members of the Charity will often share other community programs by email or newsletters. IRFAN-Canada is not unique in this. The CRA has highlighted four community events over two years that were shared by MAC members. It is the Charity’s position that this type of support, which included encouraging community initiatives such as IRFAN-Canada, was neither unlawful nor in violation of the ITA.

The CRA has highlighted 4 emails that the CRA is concerned about.

The email on December 12, 2012 and August 21, 2013 were sent by members in their personal capacity. The membership email list is used as a forum for members to inform one another about community events and news. However, the emails were sent from the members personal emails from their personal computers. Furthermore, these lists are not moderated. While the Charity expects members to adhere to ethical email practises and standards of professionalism, such emails and their content do not represent the views of the Charity.

The emails on April 15, 2012 and April 18, 2013 are also communications among staff members at Olive Grove School informing one another about a community program. Employees are allowed to use their Charity email for limited personal use as long as they follow ethical email practises and standards of professionalism. Such emails among staff members and their content do not represent the views of the Charity.

The AFL states on page 47 that “the CRA is concerned that the Organization continued to promote its relationship with IRFAN-Canada on its websites.” It is unrealistic to expect that emails written between members or staff at the Charity would be subject to scrutiny and monitoring by the Charity and would be considered to reflect the views of the Charity as if they were sent by the Charity itself. The fact that the CRA interprets emails written by members and employees that are just raising awareness about community initiatives as the Charity itself supporting the programs of IRFAN-Canada is a leap. The CRA had access to a large number of official email newsletters that were distributed by Chapters to members and members of the community, and not a single one of them contained a promotion for an IRFAN-Canada event. Having said that, the emails among staff did not breach employee code of conduct and as stated earlier IRFAN- Canada was a legitimate registered non-for-profit.

The AFL highlights an email from Mr. [REDACTED] sent on August 2, 2013. Page 46 of the AFL states that the email “explains the Organization’s policy on allowing other organizations to fundraise at its events and on its premises and why IRFAN-Canada was permitted to fundraise at its facilities and events.” The CRA is incorrect in its interpretation of this email. Mr. [REDACTED]’s email is quoted as saying “…. historically IRFAN used to collect from many years before, so we let them under special arrangement to do it very low key – but this was very specific circumstance and we already have an established relationship but we limited their scope to the most confined space possible.” This statement is equivocal. The Charity’s policy at its Eid Festival is clearly documented in the manual that sponsors are not allowed to raise funds. Sponsorship contracts do not allow for raising of funds. Up until 2011 IRFAN-Canada may have been provided an exception because of its years of sponsorship commitment. However, as of 2011 when its status was revoked, this exception was discontinued. The Charity confirms that its continued relationship up until IRFAN-Canada was listed included IRFAN- Canada’s sponsorship of MAC events, and paid rental of its facilities. The Charity dismisses that this was in any way tantamount to providing financial resources directly to IRFAN-Canada and contrary to public policy.

The AFL highlights 6 MAC events with affiliation to IRFAN-Canada. In fact, these are 3 distinct events of which 2 are sponsorship contracts. The following are some comments regarding each.

September 18, 2011 / May 12, 2013 – Olive Grove School

These were not fundraising events. IRFAN-Canada’s Annual Grand Sook of Jerusalem was a community program to bring together local businesses and cultural groups to allow community members to enjoy the food, music, art, and history of Palestinian Canadians.

This community program was within the Charity’s purpose to “to support and maintain programs and activities in order to propagate the faith of Islam,” and therefore directly contributing to advancing faith.

Palestinian Canadians represent a segment of the community members that participate in MAC’s programs and services. This event provided a direct opportunity of outreach to the community for the Charity. Many of MAC’s congregation members would participate in this event.

As a non-qualified donee, IRFAN-Canada rented MAC’s Olive Grove School once and was allowed to hold an event by paying fees. Olive Grove School did not routinely rent out its building at the time, and as a result, its rental practice required community groups using the facility to cover the costs connected with the facility’s upkeep and cleaning directly with the cleaning company.

July 14, 2012 / August 10, 2013 – Muslim Summer Festival (Ottawa)

IRFAN-Canada was one of multiple sponsors of MAC’s Summer Festival in Ottawa

The organization was invoiced and they made a payment for the 2011 Summer Festival and the 2012 Summer Festival. As for the 2013 Summer Festival they were invoiced, however, due to their status change in 2014 the outstanding amount was written off as MAC could no longer collect this receivable. However, the payment evidence provided to the CRA in Schedule “22” demonstrates that IRFAN-Canada was paying for sponsorship fees.

IRFAN-Canada did not fundraise at this event

August 18, 2012 / October 26, 2012 – GTA EID Festival (Toronto)

IRFAN-Canada was one of multiple sponsors of the Charity’s GTA Eid Festival.

Muslims celebrate Eid twice a year. Eid al-Adha is celebrated on the 10th day of the 12th and final month in the Islamic calendar. Eid al-Fitr is celebrated on the first day of the 10th month in the Islamic calendar.

A sponsorship contract covered both Eid Festivals organized by the Charity. IRFAN-Canada was invoiced for $1500.00 and made the payment, which has been provided in Schedule “22”. In the list of sponsors provided to the CRA during the audit, IRFAN was listed twice for the same event in error, once for $6000 and second time for $1500. The latter was incorrect. The invoice and payment has been provided for IRFAN-Canada’s sponsorship in 2012.

As part of the event rules and the sponsorship contract, sponsors were not allowed to raise funds. IRFAN-Canada did not fundraise at this event.

Support for the Egyptian Revolutionary Council (ERC)

The CRA has relied upon information that is significantly outside the Audit Period. The CRA has taken a position that the ERC “appears to be encouraging violence” based on biased information reported by the Egyptian Embassy in Ottawa. The Egyptian Embassy is an extension of the Egyptian regime which is responsible for overthrowing the democratically elected president and gross human rights violations including the killing of over 1,150 peaceful protestors, the detention of over 60,000 political prisoners, and mass executions and torture.125 The Charity is concerned about the CRA’s perspective that promotes the self serving narrative of the Egyptian government and undermines the reality of the human rights conditions of that country. Furthermore, the AFL has not demonstrated any evidence that either the ECCD or ECHO, both Canadian organizations that advocate for human rights and support for democracy, have ever expressed support for violence or hate.

Furthermore, the Charity reaffirms its position that allowing community groups such as ECCD and ECHO whose members are regular congregation attendees of the Charity’s centre to use the facility without payment is not indicative of the Charity being “supportive of the ECCD and ECHO’s purpose in general” as insinuated by the CRA, and certainly drawing a 3rd degree relationship to ERC is a leap.

MAC rejects this conclusion. ECCD and ECHO’s use of MAC premises is responded to earlier. Furthermore, as explained above, CRA’s view that the ERC is a group that appears to be engaging in or promoting violence is unsubstantiated and a bias of CRA towards the military coup in Egypt.

Syrian Muslim Brotherhood and Fundraising for Syria

At page 51 the AFL states, “A thorough review of the Organization’s email accounts raises our concerns about the Organization’s association with high ranking members of the Syrian Muslim Brotherhood (SMB) by certain directors and employees of the Organization.” The AFL also states on page 53 that “While the CRA does not have any information to indicate that the Organization has provided any resources to the SMB, the fact that key members of the Organization received electronic communication from the SMB is a concern as it is in direct contradiction to the Organization’s representations that it has no “connection with any Muslim Brotherhood outside of Canada or that it receives guidance from any organization.”

This is another example of the CRA drawing conclusions from the mere receipt of emails to a public account ed@macnet.ca. The Charity and the Executive Director are not responsible for unsolicited emails. Not a single example provided in the AFL is a personalized email to the Charity, in fact all of them are mass emails that included the Charity’s publicly available email account. What the CRA should be drawing judgment on is whether the Charity responded or acted upon the emails. The Charity did not, and the CRA has not been able to present a single example to demonstrate otherwise.

The AFL further alleges “It is extremely concerning that the Organization would be associating with individuals that are actively promoting and soliciting weaponry and ordnance,” in relation to the SMB. However, there is no basis to claim any association based upon the mere receipt of emails.

Appendix G – Emails

Page 52 of the AFL states “In light of the SMB’s apparent involvement in the violence occurring in Syria, it is concerning that members of the Organization received electronic correspondence from email accounts associated with several high ranking SMB figures. Please see Appendix G for a summary of the emails related to the SMB.”

In this Appendix the CRA highlights 27 emails from an individual named Ali Issa to president@macnet.ca from 96,000 emails downloaded by CRA. There is not a single example in which the owner of this email account has responded to the sender, Ali Issa. CRA has not shown a single example where the President has forwarded or acted in any way on the emails whether personally or reflected in the Charity’s activities. If there was any relationship or association, it would be expected that at least once, the owner of president@macnet.ca would have acknowledged receipt or responded.

Furthermore, there is not a single example where the sender’s email has personally addressed the President of MAC by name. All of the emails are unsolicited mass emails.

There is also another instance where the CRA has accessed personal emails of individuals on page 5 of Appendix G. This is inappropriate and the personal activities of individuals have no bearing or influence on the Charity and should not have been downloaded or included in the audit results.

Mr. [REDACTED]

The CRA alleges at page 52 of the AFL that, “Of note, one of the WATAN events held at the Organization’s Olive Grove School (OGS) on February 2, 2013293 was a seminar which was featuring [REDACTED], “member of the Syrian National Council.”

Mr. [REDACTED] is a well-regarded Canadian citizen, Muslim community leader, and member of the Charity. He has served in the leadership of many respected Muslim organizations and is a member of the Canadian Council of Imams and the Muslim World League.

Mr. [REDACTED] is a Canadian of Syrian origin and like many others responded to the Syrian crisis by educating the public on the human rights tragedy and the humanitarian crisis.

The AFL at page 57 makes two statements concerning Mr. [REDACTED]:

“It is unclear why [REDACTED], a person with no overt position of authority within the Organization, appears to be coordinating the collection and transfer of the Organization’s funds to entities unknown in Jordan and Syria.”; and

“The CRA audit was unable to confirm where this money came from, and more importantly, where it ended up.”

His emails to other members of the Charity offering options for supporting the humanitarian crisis were in his personal capacity and did not represent the organization. No money from the Charity was transferred. The CRA downloaded over 1 million financial transactions and should have been able to demonstrate if any funds were sent abroad for any cause including Syria. The CRA has also not been able to demonstrate any transaction between MAC and unapproved fundraising alternatives such as emails from individual members or external parties.

Mr. [REDACTED]’s email stating, “The person in charge of collecting donations for Syria is brother [REDACTED] ([REDACTED]),” is in reference to supporting displaced Syrian refugees with used clothing.

Mr. [REDACTED]

The AFL alleges on page 53 that, “On July 25, 2012, the Organization’s Executive Director received an email from [REDACTED], one of the Organization’s founding directors. Sent to the Executive Director’s email, ed@macnet.ca, the email appears to have been originally sent from [REDACTED] and the Independent Syrian Islamic Movement, pleading for support for Syrian revolutionary soldiers in battle.”

[REDACTED] is a Canadian citizen and was a member of the Charity. He moved abroad in 1999. He has had no membership, role or influence on the organization since he left. The fact is that the Executive Director of the Charity did not respond to him or act on this email in any way.

WATAN

The AFL states at page 54 that, “[t]he Organization appears to have supported an organization called WATAN or WATAN Syria that has been fundraising in the Organization’s premises in support of Syria.” On the same page the AFL states, “Some of the activities appear to have been conducted in conjunction with Human Concern International (HCI) while others appear to have been done solely by WATAN. The presence of another registered charity, HCI, does not absolve the Organization of its obligation to conduct due diligence on the WATAN.”

The Charity did conduct due diligence on this matter. WATAN was a Canadian project established by individuals in the community to educate the public about the humanitarian crisis in Syria. WATAN clearly states that the project was founded in collaboration with Human Concern International (HCI).126 HCI was a registered Canadian charity and a qualified donee at the time. HCI was actively fundraising for Syria and it had partnered with WATAN to educate Canadians on the situation in Syria.

As mentioned, WATAN is not a charity. It was not allowed to fundraise in any of the Charity’s facilities. All of WATAN’s independent events were community programs and information sessions. The Charity has no reservation that WATAN held an information session with Mr. [REDACTED]. As mentioned, [REDACTED] is a well regarded Canadian Muslim leader and a MAC member.

The examples of fundraising events were co-hosted by WATAN and Human Concern International (HCI). All funds were collected by HCI independently. The Charity’s due diligence was conducted with respect to HCI. The charity advises that no funds were provided to or raised by WATAN.

Syrian Active Volunteers (SAV)

The AFL at page 56 alleges “The Organization permitted the group Syrian Active Volunteers (SAV) to operate out of the Islamic Community Centre of Ontario (ICCO).”

SAV Syria used unrenovated space at the Islamic Community Centre at 2550 Dunwin Drive in Mississauga to collect clothing for refugee newcomers as part of Canada’s resettlement of 25,000 Syrian refugees. The use of the property lasted three months from January 1, 2016 to March 24, 2016.127 The Agreement has been provided at Schedule “24”.

SAV approached the Charity to run a program to support Syrian refugees. Organizations, charities, churches among others were all actively working to support the influx of refugees. This was important for the Charity and aligned with its charitable purposes. As such MAC agreed to allow SAV to use its empty warehouse space.

This program was not organized in isolation. The MAC chapter was monitoring the program and MAC volunteers were involved. It was a basic operation. Community members would drop off used clothing and items, and refugees would pick up.

As per the Charity’s due diligence, SAV Syria was recognised by the Canadian Government.128 Their positive work and clothing collection program was reported by the media.129 The Charity found it to be acceptable to allow SAV to use its facility for a short period of time of three months until it could find a permanent location. This was in the public interest as there was significant demand from Canadians to donate and support Syrian refugees arriving in the country.

The CRA raises a general concern related to organization’s involvement in humanitarian aid or refugee support for Syrians. However, Canadian humanitarian organizations called for all Canadians to support Syrians impacted by the conflict. Between September 2015 and February 2016, Canadians generously donated a total of $31.8 million to the Syria Emergency Relief Fund to support humanitarian relief efforts in response to the conflict in Syria, which the Government of Canada matched.130

The Canadian Muslim community played a front and centre role to support Syrians impacted by the uprising. Many mosques on Fridays called for Canadians to donate. Muslim relief organizations promoted donations to match government funding or independent projects in support of the humanitarian crisis.

The Charity received hundreds of emails calling for support for Syria. It is disingenuous that the CRA selected one unsolicited email and included it in the AFL on page 54 because it had the text “Save Syria” / “Support Syria” / “Syria needs your support” / “Inciting support for the just Syrian cause from all possible public and private charitable organizations.” This email was never responded to, and was one of many emails related to the Syria ordeal.

AFL Position Is Inconsistent with the Government of Canada

Despite the fact that the Charity does not engage in foreign activities, the AFL makes an effort to connect the Charity with international organisations or events.

In referring to global events, international organizations, and certain countries, the AFL makes allegations that are inconsistent with Government of Canada and are influenced by political viewpoints, particularly some that are rooted in anti-Muslim sentiments.

Taking the Syrian revolution as an example, the AFL is concerned about unsolicited emails that express support and solidarity with the Syrian people in the struggle to oppose the aggression of the Syrian Regime and Bashar Al Assad.

The Free Syrian Army (FSA) was founded by Syrian military defectors who refused to attack peaceful protestors on the orders of Bashar Al Assad. Canada has given $5.3-million to the Syrian opposition to support the rebels in anti-government propaganda since April 2012, according to the Department of Foreign Affairs (DFAIT).114 In May 2013, the European Union lifted a 2011 arms embargo on Syria. Several EU members wanted to be able to send weapons to rebel groups in order to speed up regime change and oust Bashar al-Assad. Since then, France, the United States, Qatar, Saudi Arabia, Turkey and others, have provided arms to the FSA. The Syrian National Council (SNC) was recognised or supported in some capacity by 17 UN member states, with three of those being permanent members of the Security Council as the legitimate representative of the Syrian people in the midst of the Syrian Civil War. It was also recognised by the European Union, the International Union for Muslim Scholars, and the Arab League.115 Foreign Minister John Baird, in a December 16 2011 speech in the House of Commons stated, “Assad will fall. The government will fall. It’s only a matter of time”. Later that day, Baird met with a Syrian National Council delegation led by Council President Burhan Ghalioun. The council expressed its gratitude for Canada’s assistance to the SNC, including international lobbying for new UN Security Council resolutions and its rejection of the Assad government. Discussions were held on Canada’s participation in humanitarian assistance during a transitional period and in the rebuilding of a post-Assad Syria.116 Foreign Affairs Minister John Baird expanded sanctions to include 22 more individuals associated with the Assad regime and seven companies.117 The AFL raises concern why the Organization would receive unsolicited emails that discuss the apparent involvement of the Syrian Muslim Brotherhood and the FSA in the violence occurring in Syria. The CRA’s partisan view of these groups is inconsistent with the diplomatic role of the Canadian government.

When it comes to Palestine, the AFL expresses concern regarding remarks made by individuals, rather than the Charity, in opposition to the occupation of Palestine and human rights violations committed by the State of Israel. Global Affairs Canada has always maintained a consistent foreign policy towards Palestine and Israel. The Ministry states “Canadian foreign policy objectives in the Middle East are the foundation for international assistance programming in the West Bank and Gaza.

Canada is committed to the goal of a comprehensive, just and lasting peace in the Middle East. This goal supports the creation of a viable, independent and democratic Palestinian state living side by side in peace and security with Israel. Canada believes that peace can only be achieved through a two-state solution negotiated directly between the parties.”118 The Government of Canada at the United Nations has voted in favor of the right of the Palestinian people to self- determination.119

Furthermore, the AFL relies upon comments made by the Egyptian Embassy in Canada to support its conclusions, particularly on sections related to the Egyptian revolution and Egyptian pro-democracy groups. The Egyptian Embassy is an extension of the Egyptian regime, which is responsible for overthrowing a democratically elected president and the massacre and torture of civilians. Two large sit-ins in Cairo and smaller protests across Egypt took place to denounce the military takeover and demand the reinstatement of President Morsi. In response, it is this same Egyptian government that ordered forces to repeatedly open fire on demonstrators, killing over 1,150. It is the worst massacre in Egyptian history.120

Furthermore, the Egyptian Embassy in Ottawa is also responsible for bringing and hosting Egyptian Minister Nabila Makram in Canada, who told an audience in Mississauga, Ontario, that anyone speaking “against Egypt abroad” will be “punished.” A video of Makram’s comments shows her making a slicing motion across her neck while making the remark.121 This comes after Egypt’s well documented record of arbitrary detentions, violence against political opponents and other human-rights abuses since General Abdel Fattah al-Sisi (who was famously referred to by President Trump as “my favorite dictator”122) seized power via a military coup.

In response to this incident Canada’s then former Foreign Affairs Minister Chrystia Freeland stated “Canada continues to support the desire of the Egyptian people for democracy, human rights, the rule of law and greater economic opportunity. The rights to free speech and expression are fundamental to democracy and our government will always defend Canadians – and people around the world – in their ability to exercise these rights.”123

The CRA should have exercised greater caution rather than relying on reports from a foreign government with such an atrocious record of brutality against its own citizens and whose state-controlled media outlets routinely portray Muslim community groups in the West as a threat.

2015 Board Retreat

The AFL relies extensively on the minutes of a September 2015 “Board Retreat,” yet it misrepresents both the context, the discussion and outcomes of this meeting.

First of all, this was not a Board Retreat. It was a meeting called by the Board of Directors and a cross section of members based on background, gender, age, etc. were selected to participate. The meeting invitation states

The Board of Directors has invited you to participate in a retreat to engage in both a broad and an in-depth discussion regarding our Islamic presence in the current environment. The need for such a discussion is precipitated by ongoing public relations issues facing the organization. We have ongoing issues with negative media reports and a changing political environment. We are being defined by others rather than by ourselves.” (Sent by the chair of the Board to the attendees.)

The minutes reflect a Strengths, Weaknesses, Opportunities, and Threats (SWOT) brainstorming exercise of challenges and threats. Considering the domestic and foreign anti-Muslim campaigns that the Charity was experiencing at the time, and the actions taken by the UAE to list Muslim civil society organizations in the West as terrorist groups, it would have been either extremely naive or unconscionably irresponsible of the leadership of the Charity to not address the reputational risk to the organization. To be very clear, attendees of the retreat were not worried about the Charity being listed as a terrorist organization in Canada, rather the impact of Islamophobia on the organization.

Organizing a retreat to examine the Charity’s internal and external communications around the relationship with the Muslim Brotherhood and the nuances of referring to the organization versus referring to the movement versus referring to the thought and ideas, was and is the minimum appropriate action to be taken in this regard.

The retreat was informed by both legal and public relations advice. Both advised the Charity that the international characterization of the Muslim Brotherhood organization, even with no links to MAC, would have ramifications due to shared ideology. It is ironic that CRA raises concern about this retreat and its scope in the context of “failure to conduct due diligence” because the primary objective of the retreat was to ensure due diligence.

The Charity has never been concerned about its activities with regard to the criteria for being listed as a terrorist organization. The Charity has always been concerned about the domestic and foreign Islamophobia campaigns that could impact it in Canada or abroad. The Charity was in fact transparent with CRA and communicated several times, as explained earlier and confirmed through ATIPs, that the Charity was available to discuss with the CRA the false media stories and the Islamophobic reports that were being published.

The AFL also states at page 18 that, “The decision to focus on the core ideas of Imam Al-Banna as opposed to the Muslim Brotherhood philosophy appears to be a decision made at the September 12-13, 2015 Board of Directors retreat.” This was never a decision at the retreat. The meeting did not have the authority to make any such decision. Also, the scope of discussion was around articulation and not changing the Charity’s roots and identity. The minutes of the retreat were not formal and not approved by the Board. Many of the noted comments in the minutes were simply the opinion of attendees in the context of a discussion and were not necessarily points of consensus. There were many other points of view, and this was only one attendee’s point of view. However, the conclusions were taken back to the Board for consideration.

Having said that, the CRA had the agenda of the meeting which clearly stated the subject for discussion in the 2nd agenda item which stated, “Given the current national and international environments, do you see our definition of “who are we” causing serious internal or external challenges in terms of misunderstanding, wrong interpretations, political or public media pressures.” The AFL extracted the above text from the minutes and removed it from its original context. The minutes state “There was some apprehension about us not continuing to include HB and/or MB in our identity definition as, the argument goes, it would eventually lead to the eventual diminishment of our core values and principles.” The discussion was never about concern about activities that are problematic, or removing connections to external organizations, but about how to effectively describe the Charity with respect to the Muslim Brotherhood in its website, bylaws, and other publications.

The opinion developed by the CRA in the AFL concerning the retreat demonstrates a misconstrued and manifestly unfair approach to the audit. The retreat was called in fact to ensure due diligence and provide clarity to internal and external stakeholders. Recommendations were acted upon by the Board with transparent changes to the bylaws, the website and other materials. This process should have provided CRA with confidence that the Charity was taking necessary steps to ensure that the organization and how it articulates itself is in accordance with public policy.

Anti-Terrorism Policy (ATP)

In the summary found at page 58 the AFL states

“After a review of the Organization’s records and representations, the CRA found that despite having created an Anti-Terrorism Policy (ATP) in 2011, it appears as though the Organization never implemented the document in a truly meaningful manner and has failed to demonstrate that it conducts meaningful due diligence. The failure to conduct due diligence, whether purposeful or negligent, has resulted in several of the Organization’s activities being considered by the CRA to be activities contrary to public policy.”

The Charity developed its first Anti-Terrorism Policy and further developed an Adherence and Due Diligence Package which is current as of December of 2015.

This package outlines the Charity’s policies and position on various issues, including Anti- Money Laundering and Terrorist Financing. Relevant sections of this Package are as follows:

Extremist ideologies are inconsistent with our values as Canadian Muslims. Through our efforts to promote civic awareness and duty we try to educate and train our youth to bring positive change, thwarting the efforts of radicalization across the country.

The Charity operates a number of full-time schools across the country, preaching moderation and the contemporary practise of Islam. These schools have a strong curriculum approved by Governments across Canada.

The Charity is committed to the safety of its premises, students, staff, members and visitors and above all compliance with all relevant laws.

The Charity has developed policies, practises and procedures related to Anti-Terrorism, to ensure that the above commitment is being met.

The Charity is also committed to working with stakeholders in Government law enforcement and other faith groups to improve on these procedures. The Charity will continue to update these policies and procedures to ensure they remain current, effective and aligned with any new laws.

The MAC Anti-Terrorism Policy includes the following:

General Policy Guidelines and Principles

Risk Management

Governance Accountability and Transparency

Reporting

Program Review

Donor Review

Financial Transparency

Review of Participants

Review of Associates

Proceeds of Crime (Money Laundering) and Terrorist Financing Act

An Anti-Terrorism checklist was also developed to ensure that programs undertaken by MAC do not compromise its charitable status by contravening Anti- Terrorism Legislation. In this respect, a program under review should not involve or appear to involve the association with terrorist activities, terrorist groups or in facilitating terrorist activities or terrorist groups. MAC has provided a copy of an Anti-Terrorism Due Diligence Program Review conducted in the audit period attached again at Schedule “23”.

The Charity has in fact applied its anti-terrorism policy using an objective approach in judging a group’s risk based on legitimate reliable sources, specifically the Canadian, US, EU, and UN terrorist lists, rather than online hearsay, third party sources, and misinformation. This is important to ensure that the Charity does not prejudice an organization doing important work. It is unreasonable for CRA to expect a charity to investigate “perceived links”, as the Charity can only rely on accessible government resources and reliable third-party providers to determine legitimate links to terrorist activities.

It’s important to note that the Charity’s donor community grew by 28% in 2013, 18% in 2014, and 18% in 2015 as shown below. These accounted for thousands of donation transactions. The AFL has not pointed out a single transaction or donor that it is concerned about for risk or identified “perceived links” despite the large number of donors and transactions.

At page 40, the AFL notes, “In order to prevent the charity’s resources from being used in a manner that would contravene Canadian law and the charity’s requirements for ongoing registration, a registered charity should conduct meaningful due diligence on all aspects of its operations. This would include ensuring that a charity does not operate in association with individuals or groups that are engaged in terrorist activities or that support terrorist activities. Links, alleged or even perceived links between a charity and terrorism are corrosive to public confidence in the integrity of charity. A significant aspect of a trustee’s legal duties to protect charitable assets means carrying out proper due diligence to give reasonable assurance about those individuals and organizations that give money to, or receive money from, or work closely with, the charity.”

First of all, it is unclear to the Charity why the CRA would reference the UK Charities Commission Guidance “OG 410 Charities and Terrorism” in explaining the Charity’s responsibility to ensure it does not contravene Canadian law and the charity’s requirements for ongoing registration. As a strictly domestic Canadian registered charity, the organization is not responsible to seek guidance or compliance with Charity regulators of foreign countries.

Nevertheless, in 2011 the Charity’s Board of Directors approved the Charity’s Anti-Terrorism policy to protect the Charity’s assets from abuse. The policy accounts for those individuals and organizations that give money to, or receive money from, or work closely with, the charity.

As it relates to donors the Charity’s policy requires that “A reasonable sampling of all new or proposed donors or donations less than $10,000.00 shall be subject to an initial review. All new or proposed donors or donations greater than $10,000.00 shall be subject to an initial review, and all existing Donor-lists shall be subject to review as required.” This policy has been implemented by MAC and demonstrated to the CRA.

In our letter of December 21, 2018 attached as Schedule “11”, the following clarification was provided:

“During the course of the head office visit between February 29, 2016 and March 1, 2016, questions were raised concerning the application of MAC’s anti-terrorism policy. At that time, the audit interview notes reflect that the executive director appeared to indicate that anti-terrorism policy is not consistently applied. For certainty, MAC is consistent in the application of the anti-terrorism policy in the course of its activities. This is applied across the entire organization, and is monitored and managed by the head office…

In relation to the fundraising activities of MAC discussed above, all donors and donations are subject to review by the anti-terrorism committee (currently made of the Director of the Fundraising, the Controller, and the Executive Director) to determine, to the extent possible, whether they are compromised by any connection or appearance of connection with Terrorist Activity, Terrorist Groups, or Facilitating Terrorist Activity or Groups or whether they may be otherwise in violation of the Anti-Terrorism Legislation, including the Proceeds of Crime (Money Laundering) and Terrorist Financing Act.

All donor reviews, whether of new or existing donors, are conducted in accordance with the Donor Review Check-List attached to MAC anti-terrorism policy as per Schedule C. Therefore, all donors making donations of $10,000 or more are screened against a variety of international and country-sponsored Watch lists, while donations of less than $10,000 are sample-screened through a randomized sampling.

A reasonable randomized sampling (about 1 % of transactions) of all donors or donations less than $10,000.00 are subject to similar checks and reviews.

No positive identification has occurred to date. However, in the event that a donor or donation is compromised by real or possible links to Terrorist Activities or Terrorist Groups, MAC shall not accept the donation, or any further donations as the case may be, from the donor. The donation shall be returned to the donor along with a brief explanation that MAC is unable to accept the gift where possible at law after consultation with legal counsel. MAC shall keep a copy of the documentation, concerning the donation, on file.

Further, our client has provided the Canada Revenue Agency Auditors a list of checks that the organization performs based on the individual’s role in the organization.”

This clarification has effectively been ignored by the CRA.

Povrel Jerusalem Fund for Human Services (JFHS) and The Canadian Middle East Information Centre (CMIC)

The Charity is concerned about the CRA including allegations against The Canadian Middle East Information Centre (CMIC) of spreading propaganda that have never been proven. The CRA bases its allegation on the fact that in an Immigration Refugee Board (IRB) process the “CMIC acknowledged that it distributes two Islamic newspapers.” (Appendix F) This is in fact not true.

Referring to the original text of the IRB testimony, the allegations presented before the IRB are by an unknown source and not by CMIC.124 There is nothing provided to support the allegations made by the CRA.

As it relates to the Povrel Jerusalem Fund for Human Services (JFHS), CRA’s accusations concerning the relationship between JFHS and IRFAN-Canada is simply an attempt to draw some degree of influence on the Charity between it and IRFAN-Canada.

The AFL alleges at page 45 that

“As detailed in Appendix F, some of the Organization’s most prominent members, directors, and officials were either involved in IRFAN-Canada, or a network of charities that appear to have been used to propagate and fundraise for Hamas in Canada. The involvement of the directors/employees in an apparent Hamas support network is troubling and may indicate why certain activities, such as the continued support for IRFAN-Canada, were undertaken by the Organization.”

The CRA in this appendix attempts to demonstrate that since some individuals associated with the Charity served as board members with JFHS or CMIC prior to 1999 and before MAC was ever registered, it is evidence that there existed influence on the Charity to provide support/resources to IRFAN-Canada a decade later. The members of the Charity have always been active members in their community. It should be no surprise that they are active in other organizations within the community before and after the Charity was founded. The linking of individuals or directors who served or serve on other organizations to allegations of influence on the decisions, policies, and activities of the Charity is completely speculative.

The Charity has never interacted with JFHS or CMIC. It interacted strictly with IRFAN-Canada, which was not listed by Canada, the US, the EU or the United Nations as an organization of concern until 2014.

Support for International Relief Fund for the Afflicted and Needy (IRFAN- Canada)

At page 45 of the AFL, the CRA alleges that, “An analysis of audit documentation and publicly available sources suggests that the relationship between the Organization and IRFAN-Canada not only continued after the suspension of IRFAN-Canada’s registered status but well after its revocation for, in part, supporting the listed terrorist entity Hamas.” As well, on pages 45 and 46 CRA states that, “In addition to permitting IRFAN-Canada to use the Organization’s events and resources to collect funds, the Organization’s electronic resources appear to have been used to further IRFAN-Canada’s interests and agenda.” and “The Organization appears to have held several events where IRFAN-Canada was given an opportunity to promote itself and raise funds for its various programs.”

As explained, MAC’s institutions are used by the community and open to the community for external activities, for example community iftars, Eid gatherings, baby shower sermons, and other gatherings. This is similar to other faith groups.

Between 2011 and 2014 IRFAN-Canada remained a non-qualified donee as a non- profit organization. As a non-qualified donee, IRFAN-Canada rented MAC’s Olive Grove School and was allowed to hold an event by paying fees. Olive Grove School did not routinely rent out its building at the time, and as a result, its rental practice required community groups using the facility to cover the costs connected with the facility’s upkeep and cleaning directly with the cleaning company. To be clear, this permission was withdrawn as soon as IRFAN-Canada was included on the government of Canada’s list of terrorist organizations in April, 2014.

In other instances, IRFAN-Canada paid sponsorship fees to support the Charity’s events and in return received acknowledgement for its sponsorship. The ITA does not restrict a non-qualified donee from using the resources of a registered charity for fair market value. During this period in which it was a non-qualified donee, IRFAN-Canada has never raised funds in the Charity’s facilities or events. As noted above, the AFL references a YouTube video but the link provided is incorrect and cannot be verified. Also, the event links provided by the CRA in footnotes 222 and 223 are broken. While the Charity cannot verify the event description provided by the CRA, the Charity can confirm that the IRFAN-Canada was never allowed to, nor did it, fundraise in its Annual Grand Souk of Jerusalem event.

After December 2010 when the CRA revoked IRFAN-Canada’s charitable status many major Canadian organizations continued to affiliate with the organization. In 2011 and 2012 IRFAN-Canada remained a major sponsor of the Reviving Islamic Spirit Conference as well as one of the largest Muslim festivals, MuslimFest. Other Canadian mosques, of which some are registered charities, were renting their facilities to IRFAN-Canada for events. The City of Mississauga continued to rent its facilities to IRFAN-Canada for community picnics and events. In 2013 IRFAN- Canada in cooperation with The International Islamic Youth League, the United Nation High Commissioner for Refugees, the Zakat Foundation of America, the United Arab Emirates Red Crescent Society, and the Islamic Foundation of Ireland partnered to distribute humanitarian relief support to the refugees in Mali to support internally displaced persons.

The Charity rejects the conclusion that it allowed IRFAN-Canada to raise funds at real property owned by the Charity. IRFAN-Canada has never been allowed to fundraise in MAC premises. On page 46 of the AFL, the CRA raises 4 alleged incidents where this may have been the case. As a grassroots organization with access to the community, members of the Charity will often share other community programs by email or newsletters. IRFAN-Canada is not unique in this. The CRA has highlighted four community events over two years that were shared by MAC members. It is the Charity’s position that this type of support, which included encouraging community initiatives such as IRFAN-Canada, was neither unlawful nor in violation of the ITA.

The CRA has highlighted 4 emails that the CRA is concerned about.

The email on December 12, 2012 and August 21, 2013 were sent by members in their personal capacity. The membership email list is used as a forum for members to inform one another about community events and news. However, the emails were sent from the members personal emails from their personal computers. Furthermore, these lists are not moderated. While the Charity expects members to adhere to ethical email practises and standards of professionalism, such emails and their content do not represent the views of the Charity.

The emails on April 15, 2012 and April 18, 2013 are also communications among staff members at Olive Grove School informing one another about a community program. Employees are allowed to use their Charity email for limited personal use as long as they follow ethical email practises and standards of professionalism. Such emails among staff members and their content do not represent the views of the Charity.

The AFL states on page 47 that “the CRA is concerned that the Organization continued to promote its relationship with IRFAN-Canada on its websites.” It is unrealistic to expect that emails written between members or staff at the Charity would be subject to scrutiny and monitoring by the Charity and would be considered to reflect the views of the Charity as if they were sent by the Charity itself. The fact that the CRA interprets emails written by members and employees that are just raising awareness about community initiatives as the Charity itself supporting the programs of IRFAN-Canada is a leap. The CRA had access to a large number of official email newsletters that were distributed by Chapters to members and members of the community, and not a single one of them contained a promotion for an IRFAN-Canada event. Having said that, the emails among staff did not breach employee code of conduct and as stated earlier IRFAN- Canada was a legitimate registered non-for-profit.

The AFL highlights an email from Mr. [REDACTED] sent on August 2, 2013. Page 46 of the AFL states that the email “explains the Organization’s policy on allowing other organizations to fundraise at its events and on its premises and why IRFAN-Canada was permitted to fundraise at its facilities and events.” The CRA is incorrect in its interpretation of this email. Mr. [REDACTED]’s email is quoted as saying “…. historically IRFAN used to collect from many years before, so we let them under special arrangement to do it very low key – but this was very specific circumstance and we already have an established relationship but we limited their scope to the most confined space possible.” This statement is equivocal. The Charity’s policy at its Eid Festival is clearly documented in the manual that sponsors are not allowed to raise funds. Sponsorship contracts do not allow for raising of funds. Up until 2011 IRFAN-Canada may have been provided an exception because of its years of sponsorship commitment. However, as of 2011 when its status was revoked, this exception was discontinued. The Charity confirms that its continued relationship up until IRFAN-Canada was listed included IRFAN- Canada’s sponsorship of MAC events, and paid rental of its facilities. The Charity dismisses that this was in any way tantamount to providing financial resources directly to IRFAN-Canada and contrary to public policy.

The AFL highlights 6 MAC events with affiliation to IRFAN-Canada. In fact, these are 3 distinct events of which 2 are sponsorship contracts. The following are some comments regarding each.

September 18, 2011 / May 12, 2013 – Olive Grove School

These were not fundraising events. IRFAN-Canada’s Annual Grand Sook of Jerusalem was a community program to bring together local businesses and cultural groups to allow community members to enjoy the food, music, art, and history of Palestinian Canadians.

This community program was within the Charity’s purpose to “to support and maintain programs and activities in order to propagate the faith of Islam,” and therefore directly contributing to advancing faith.

Palestinian Canadians represent a segment of the community members that participate in MAC’s programs and services. This event provided a direct opportunity of outreach to the community for the Charity. Many of MAC’s congregation members would participate in this event.

As a non-qualified donee, IRFAN-Canada rented MAC’s Olive Grove School once and was allowed to hold an event by paying fees. Olive Grove School did not routinely rent out its building at the time, and as a result, its rental practice required community groups using the facility to cover the costs connected with the facility’s upkeep and cleaning directly with the cleaning company.

July 14, 2012 / August 10, 2013 – Muslim Summer Festival (Ottawa)

IRFAN-Canada was one of multiple sponsors of MAC’s Summer Festival in Ottawa

The organization was invoiced and they made a payment for the 2011 Summer Festival and the 2012 Summer Festival. As for the 2013 Summer Festival they were invoiced, however, due to their status change in 2014 the outstanding amount was written off as MAC could no longer collect this receivable. However, the payment evidence provided to the CRA in Schedule “22” demonstrates that IRFAN-Canada was paying for sponsorship fees.

IRFAN-Canada did not fundraise at this event

August 18, 2012 / October 26, 2012 – GTA EID Festival (Toronto)

IRFAN-Canada was one of multiple sponsors of the Charity’s GTA Eid Festival.

Muslims celebrate Eid twice a year. Eid al-Adha is celebrated on the 10th day of the 12th and final month in the Islamic calendar. Eid al-Fitr is celebrated on the first day of the 10th month in the Islamic calendar.

A sponsorship contract covered both Eid Festivals organized by the Charity. IRFAN-Canada was invoiced for $1500.00 and made the payment, which has been provided in Schedule “22”. In the list of sponsors provided to the CRA during the audit, IRFAN was listed twice for the same event in error, once for $6000 and second time for $1500. The latter was incorrect. The invoice and payment has been provided for IRFAN-Canada’s sponsorship in 2012.

As part of the event rules and the sponsorship contract, sponsors were not allowed to raise funds. IRFAN-Canada did not fundraise at this event.

Support for the Egyptian Revolutionary Council (ERC)

The CRA has relied upon information that is significantly outside the Audit Period. The CRA has taken a position that the ERC “appears to be encouraging violence” based on biased information reported by the Egyptian Embassy in Ottawa. The Egyptian Embassy is an extension of the Egyptian regime which is responsible for overthrowing the democratically elected president and gross human rights violations including the killing of over 1,150 peaceful protestors, the detention of over 60,000 political prisoners, and mass executions and torture.125 The Charity is concerned about the CRA’s perspective that promotes the self serving narrative of the Egyptian government and undermines the reality of the human rights conditions of that country. Furthermore, the AFL has not demonstrated any evidence that either the ECCD or ECHO, both Canadian organizations that advocate for human rights and support for democracy, have ever expressed support for violence or hate.

Furthermore, the Charity reaffirms its position that allowing community groups such as ECCD and ECHO whose members are regular congregation attendees of the Charity’s centre to use the facility without payment is not indicative of the Charity being “supportive of the ECCD and ECHO’s purpose in general” as insinuated by the CRA, and certainly drawing a 3rd degree relationship to ERC is a leap.

MAC rejects this conclusion. ECCD and ECHO’s use of MAC premises is responded to earlier. Furthermore, as explained above, CRA’s view that the ERC is a group that appears to be engaging in or promoting violence is unsubstantiated and a bias of CRA towards the military coup in Egypt.

Syrian Muslim Brotherhood and Fundraising for Syria